How States Tax Cannabis — And Why Montana’s System Stands Out

Ironleaf Law Firm

Cannabis taxes across the United States range from simple percentage-of-sale systems to elaborate weight-based formulas that resemble agricultural commodity pricing more than retail taxation. Some states treat cannabis like alcohol, others like tobacco, and a few still treat it like contraband. Understanding these differences matters because tax structure directly shapes whether a legal market thrives, stagnates, or collapses under its own weight.

Montana’s system is often described as “straightforward,” but compared to the rest of the country, it’s more accurate to call it lean, high-rate, and unusually dependent on retail-level taxation. That combination has real consequences for consumers, businesses, and the long-term stability of the market.

This post walks through the major tax models used across the country, highlights which ones work (and which don’t), and offers a candid look at where Montana fits in—and why the market behaves the way it does.

1. The Three Major Cannabis Tax Models in the U.S.

A. Weight-Based Taxes: Cannabis as a Crop

Some states tax cannabis by the gram, ounce, or pound—similar to agricultural commodities.

- Alaska: “An excise tax of $50 per ounce… on marijuana sold or transferred from a marijuana cultivation facility” (Alaska Stat. § 43.61.010).

- Alabama, Georgia, Idaho: $3.50 per gram of marijuana, regardless of purity (Code of Ala. § 40-17A-8; O.C.G.A. § 48-15-6; Idaho Code § 63-4203).

Strengths: predictable revenue, stable for state budgeting.

Weaknesses: ignores market price; can crush cultivators when wholesale prices fall.

B. THC-Based Taxes: Cannabis as a Potency-Driven Product

A newer model taxes cannabis based on THC content.

- Connecticut: $0.00625/mg THC for flower; $0.0275/mg for edibles; $0.009/mg for other products (Conn. Gen. Stat. § 12-330ll).

- Illinois: Higher excise rates for higher-THC products (410 ILCS 705/65-10).

Strengths: aligns tax with potency; discourages ultra-high-THC products.

Weaknesses: requires precise testing; creates incentives for lab shopping.

C. Percentage-of-Price Taxes: Cannabis as a Retail Consumer Good

This is the most common model—and the one Montana uses.

- California: 15% excise tax on retailer gross receipts (18 CCR 3801; Cal. Rev. & Tax Code § 34011.2).

- Delaware: 15% retail tax (4 Del. C. § 1382).

- Illinois: 7% wholesale tax + 10–25% retail excise taxes (410 ILCS 705/60-10; 410 ILCS 705/65-10).

Strengths: easy to understand; scales with price.

Weaknesses: high rates push consumers back to the illicit market.

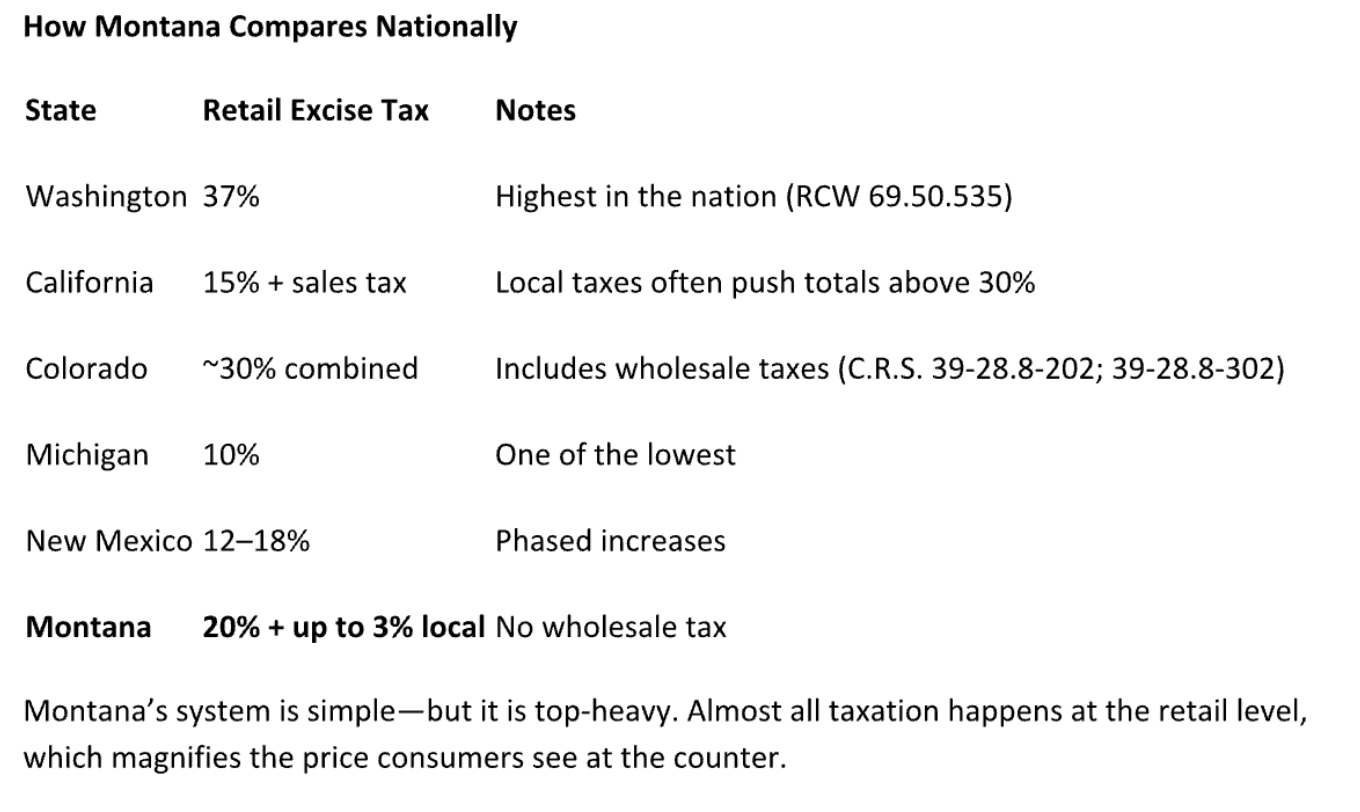

2. How Montana Taxes Cannabis

Montana uses a percentage-of-price model, but with unusually high retail rates:

- 20% adult-use tax

- 4% medical tax

- Up to 3% local option tax (M.C.A. §§ 15-64-102, 16-12-310(1))

This puts the total adult-use burden at 23% in many counties, and up to 26% where both county and municipal taxes apply.

3. What Works (and Doesn’t) in Other States

A. High-Tax States With Persistent Price Pressure

California and Washington impose some of the highest statutory tax burdens in the country.

- California’s 15% excise tax is “in addition to sales and use tax imposed by the state and local governments” (Cal. Rev. & Tax Code § 34011.2).

- Washington’s 37% excise tax applies to every retail sale (RCW 69.50.535).

These statutes create effective tax burdens exceeding 30% in California and 37% in Washington. Because illicit markets pay none of these taxes, the statutory structure itself creates a significant price gap between legal and illegal products—an economic reality that allows illicit markets to remain competitive.

B. Moderate-Tax States With Stable Markets

Colorado, Michigan, and Oregon show that moderate taxes + predictable rules = functional markets.

- Colorado exempts medical transfers from excise tax (C.R.S. 39-28.8-302(2)).

- Michigan’s 10% excise tax helped drive prices down and legal participation up.

C. Complex Systems That Slow Down Market Growth

Connecticut and Illinois have sophisticated but burdensome systems.

- Connecticut’s THC-based tax requires precise testing and complex accounting (Conn. Gen. Stat. § 12-330ll).

- Illinois’ multilayered wholesale + retail + local taxes create high consumer prices and heavy compliance costs (410 ILCS 705/60-10; 65 ILCS 5/8-11-23).

These statutes show multi-layered, administratively heavy systems with multiple points of taxation, indicating that such systems generate revenue but slow market growth.

4. How Montana Compares: Strengths and Weaknesses Strengths

- Simple structure — easy for businesses and regulators.

- Predictable revenue — percentage-based taxes scale automatically.

- Medical preference — 4% rate keeps medical viable.

Weaknesses

- High retail burden — among the highest in the country.

- No wholesale tax — cultivators bear no tax burden; consumers see the full load.

- Price sensitivity in rural markets — high taxes + low population density = fragile margins.

- Illicit competition risk — especially near Wyoming, Idaho, and the Dakotas.

Montana’s Market Conditions in Plain Terms

Montana’s cannabis industry operates in a low-density, oversupplied market where high retail taxes and falling wholesale prices have created a highly stressed operating environment. Many businesses describe the landscape as economically depleted, with conditions that make long-term sustainability difficult, as indicated by industry reports such as the 2025 State of the Cannabis Industry Report by First Citizens Bank, which highlights challenges including high taxation, market oversupply, and price pressures squeezing profit margins. Additionally, economic analyses from Whitney Economics emphasize the fragile market conditions in rural states like Montana, where high retail taxes and declining wholesale prices create a stressed operating environment.

This is not a booming West Coast ecosystem—it’s a thin, rural market with too many operators, declining prices, and a tax structure that places nearly the entire burden on the final retail transaction.

5. What Montana Could Learn From Other States

These are not recommendations—just grounded policy alternatives drawn from what other states have tried.

A. Introduce a Modest Wholesale Tax

Many states spread the tax burden across the supply chain.

- Colorado taxes retail cultivation but exempts medical transfers (C.R.S. 39-28.8-302).

- Nevada imposes a 15% wholesale tax on the first sale (NRS 372A.290).

- Illinois imposes a 7% cultivation privilege tax (410 ILCS 705/60-10).

A small wholesale tax could reduce sticker shock at retail without reducing total revenue.

B. Reevaluate the 20% Adult-Use Rate

Montana’s rate is high for a rural state with limited population density. A reduction to 15% would still place Montana above national averages but could improve competitiveness and reduce illicit market incentives.

C. Allow More Local Flexibility

Some states allow municipalities to adjust rates based on local conditions. Montana’s flat 3% cap limits local experimentation.

D. Strengthen Medical Protections

Several states exempt medical cannabis entirely.

- Delaware: “The retail sales tax is not imposed on the sale of medical marijuana products…” (4 Del. C. § 1382).

- Florida: “Marijuana and marijuana delivery devices are exempt from the taxes imposed under this chapter” (Fla. Stat. § 212.08).

Montana’s 4% rate is low, but not zero.

6. Final Thoughts

Montana’s cannabis tax system is simple, predictable, and easy to administer—but it is also one of the highest retail tax burdens in the country, especially for a rural state with a small consumer base. Compared to other states, Montana’s model is closer to California and Washington than to Colorado or Michigan, and that has real consequences for market stability.

The next few years will reveal whether Montana’s high-rate, retail-heavy structure can sustain a healthy legal market—or whether adjustments will be needed to prevent further consolidation and business failures.